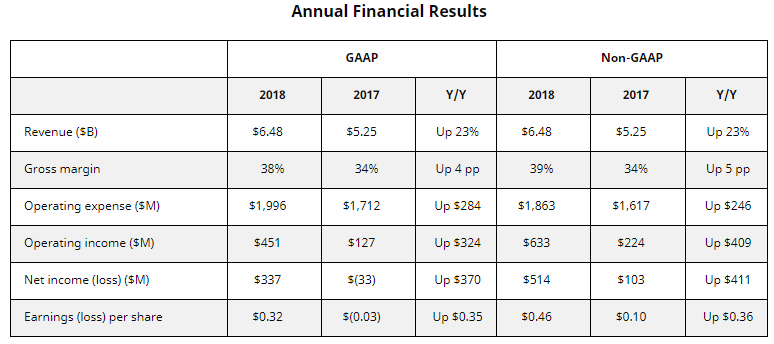

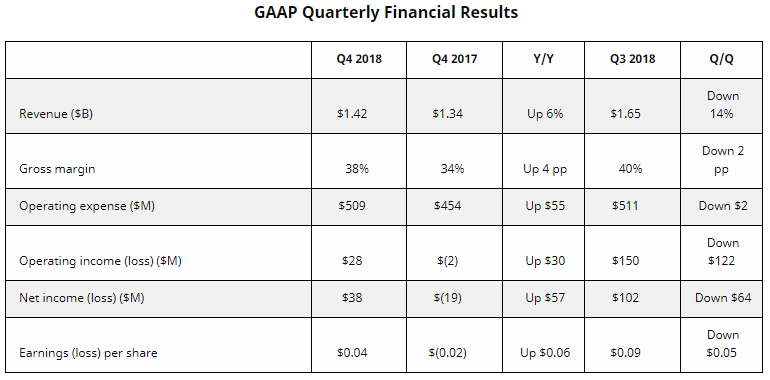

Today AMD announced their earnings for Q4 as well as the annual results of 2018. The company had revenue of $6.48 B and a net income of $337 M. This is a pretty significant improvement from 2017 with revenues of $5.25 B and a net loss of $33 M. While Intel’s quarter and annual earnings dwarf what AMD has done, the company has improved its position financially. AMD’s guidance from Q3 earnings indicated that revenue would be down for Q4 as compared to the previous quarter, and results matched those expectations. Q4 revenue came in at $1.42 B with a net income of $38 M. This fell within the range of $1.4 to $1.5 that AMD was expecting. This is compared to the relatively strong Q3 which had revenues of $1.65 B and a net of $102 M.

Annually this is probably the best overall year since 2011 for AMD. The company looks to be running quite lean and has shown that it can achieve profits even in down quarters. It also helps that AMD has been able to get much better terms from GLOBALFOUNDRIES and has successfully amended their wafer agreement so that AMD can pursue manufacturing products at other foundries at 7nm without penalty or royalty payments to GLOBALFOUNDRIES. While GF’s sub 10nm development is now shuttered, the company will still be producing 12/14nm products which will include the upcoming I/O chiplets for use with the next generation Ryzen series as well as EPYC 2. The amended agreement sets purchase targets through 2021, but the agreement itself lasts through 2024.

The primary revenue driver for the company is of course the CPU and GPU markets. Ryzen has continued to provide strong numbers for AMD and has lead to greater numbers shipped as well as higher ASPs. Years of Bulldozer based parts eroded ASPs to nearly unsustainable numbers, but the introduction of Ryzen nearly two years ago has strengthened the foundation of the company and their revenue stream. AMD has reported no inventory issues with either leftover stock of the first generation Ryzen parts or the latest Ryzen 2000 series. There is some fluidity here as EPYC processors utilize the same dies (though more heavily binned) as well as the HEDT Threadripper CPUs that have become popular in workstation applications. Multiple products at a pretty extreme price range utilizing the same basic die is a pretty good way to avoid excess inventory issues, but it is a little scary if demand picks up in one of those areas and there are not enough chips to supply these multiple product lines.

GPUs are not in as good of shape as CPUs. The crypto boom was good for the GPU market, but as soon as that dropped then AMD was left with quite a bit of inventory and a much lower demand. This is partially offset by increases in sales of datacenter GPUs, but AMD looks to be trying to get of as much of this inventory before large scale production of Navi based parts goes into full swing. Current Polaris based parts are competitive for their price points and users can expect a very solid product for the market ranges they represent.

Click here to continue reading about AMD Q4 2018 Results!

Enterprise, Embedded, and Semi-Custom saw the largest drop of the different groups. The primary negative mover here is that Q3 earnings from semi-custom royalties reflected the build-up of product from partners for the Holiday Season. Q4 royalties dropped dramatically. AMD is in a bit of a lull in terms of receiving revenue from developing next generation console chips and receiving royalties from mature and well saturated products. Offsetting this are increased EPYC sales at reasonable ASPs. There has been some debate if AMD has in fact gained any marketshare in the server market with EPYC and if they are selling them at a loss. Napkin math here makes it look as though AMD has in fact gained a slight amount of marketshare and have somewhat healthy ASPs. These are not slam dunk products like the original Opteron which powered AMD through some record quarters. Rather these are competitive parts in a market that is dominated by Intel. Rolling out new server parts takes much more verification and platform development than what we see in desktop and mobile, so AMD is not exactly where they want to be. They still are reporting that they have doubled sales from the previous quarter, and that has helped offset the loss of royalties from the group.

Anecdotally it looks like major server vendors are actively pushing their clients towards EPYC solutions due to the lead times for orders that rely on Intel’s Xeon based CPUs. A contact of mine was invited to a Dell summit in Oklahoma a few weeks ago and when the lead times for Xeon based products was discussed, the Dell sales people highly recommended moving to AMD products as they offered comparable performance and core counts for much less money. There were several groans throughout the audience as this was mentioned so it still seems that AMD has a ways to go to gain the confidence of purchasing managers and CTOs. It is good to see OEMs like Dell actively pushing AMD products, as it also helps their bottom line in moving product at a reasonable pace without having to wait for Intel to provide product to meet demand.

It does not look like AMD is making any significant gains in marketshare, but their current product stack allows them to at least keep from losing marketshare. The markets are not growing as fast as they once were, but what growth there is AMD is capitalizing on. AMD also seems more insulated from the issues that Intel is experiencing with sales in China as well as the manufacturing constraints that Intel is facing (not to mention the disastrous 10 nm migration).

Looking ahead AMD expects Q1 to be lower revenue than the previous quarter. It should come in around $1.25 B due to again lower GPU sales as well as seasonality across the business. Q1 is typically one of the lowest quarters in terms of revenues with a small rise in Q2, depending on the product stack and new introductions. AMD looks to be releasing their 7 nm CPU products around the end of 1H 2019. This includes Zen 2 based desktop and server parts. AMD had previously expected EPYC 2 products to be released in an early 2019 time frame, but this has not been the case. We do not know if this was due to design issues, 7 nm availability/maturity, or some combination of the above mentioned as well as platform issues due to the new modular CPU design.

AMD could potentially have a banner year as they look to have a full lineup of 7 nm parts that could offer a lot more value than competing Intel options. Zen 2 is a significant redesign that will enhance performance as well as utilize the advantages that TSMC’s 7 nm process has over Intel’s current 14++ product. If Intel continues to have issues getting 10 nm out the door in significant quantities by the end of 2019, AMD has a real chance to capture a significant amount of marketshare across the board. The only area that AMD would be lacking in is the mobile segment where 7 nm parts are not expected until early 2020.

This was a solid quarter and year for AMD and has shown that the company can continue to move forward even under challenging conditions. Intel still claims the vast majority of the market, but the smaller company is making inroads in markets by providing good performance at excellent prices. They are also providing impetus for Intel to change the way they have been doing things for the past decade. 2019 is certainly going to be an interesting year.

First line typo:

“as well as

First line typo:

“as well as the annual results of 2019”

Should be 2018

“results of 2019” likely

“results of 2019” likely refers to the fiscal year 2019. It is common to number a fiscal year after the calendar year in which it ends.

Well, while it is true what i

Well, while it is true what i said about fiscal year numbering, i just looked up when AMD’s fiscal year starts and ends. As it turns out, AMD’s fiscal year aligns with the calendar year. So, i have to correct myself and agree with “results of 2019” being a typo…

Here I was writing 2018 on my

Here I was writing 2018 on my checks still…

“It also helps that AMD has

“It also helps that AMD has been able to get much better terms from GLOBALFOUNDRIES and has successfully amended their wafer agreement so that AMD can pursue manufacturing products at other foundries at 7nm without penalty or royalty payments to GLOBALFOUNDRIES.”

This is a fake news since nobody excepted AMD and GlobalFoundries know the exact terms of the Wafer Supply Agreement renegociated 3 YEARS ago.

Actually, AMD paid penalties to GlobalFoundries!

“In partial consideration for these rights, AMD will:

Make quarterly payments to GF beginning in 2017 BASED ON THE VOLUME OF CERTAIN WAFERS PURCHASED FROM ANOTHER WAFER FOUNDRY.”

http://ir.amd.com/news-releases/news-release-details/amd-announces-multi-year-amendment-wafer-supply-agreement

The non penalty negotiation

The non penalty negotiation was a recent renegotiation specifically to 7nm products only. The old agreement included 7nm, and AMD has to use TSMC for that as GF shuttered their 7nm development.

Indeed I missed that

Indeed I missed that point…

“Wafer Supply Agreement Update

Today AMD announced it entered into a seventh amendment to its wafer supply agreement with GLOBALFOUNDRIES Inc. (GF). GF continues to be a long-term strategic partner to AMD for the 12nm node and above and the amendment establishes purchase commitments and pricing at 12nm and above for the years 2019 through 2021. The amendment provides AMD full flexibility for wafer purchases from any foundry at the 7nm node and beyond without any one-time payments or royalties.”

http://ir.amd.com/news-releases/news-release-details/amd-reports-fourth-quarter-and-annual-2018-financial-results

But I’m still wondering how a recent renegotiation of the WSA announced the 29 january 2019 could impact a full PAST quarter…

Once more, how Mubadala (i.e. AMD and GlobalFoundries main stockholder) expect to compensate the loss generated by the 7 nm scam from GlobalFoundries? A discretionary sale?

Abu Dhabi’s oil (and many other OPEC members) is hardly challenged by USA oil producers…

Woah there Floyd R Turbo! GF

Woah there Floyd R Turbo! GF ran their numbers and they could not afford to develop their own 7nm process. And AMD only got out from under paying cash tributes to GF for any 7nm production done at competators’ foundries and that’s because GF canned it’s 7nm process node development.

AMD has still got 12nm and 14nm production agreements that were also renewed and those first generation Zen Based Epyc/Rome chips will still be in production for a good 3+ more years on GF’s 14nm node with GF’s 12nm node used for most consumer Zen+ and Polaris CPU and GPU production. And AMD still has some GF 28nm production for some legacy embedded and Carrizo/Bristol Ridge, and A series, production for OEM/Embedded clients.

All the first generation Zen/Epyc production and Ryzen 14nm/12nm production will keep GF very busy in addition to GF making the 14nm I/O dies for Epyc/Rome and Ryzen 3000 desktop SKUs.

Wafer argeements at least guarantee AMD production capacity should any market conditions result in limited wafer start capacity at the third pary fab companies.

TSMC or Samsung will be competing for AMD’s 7nm production contracts but GF has got so much 14nm/12nm, and 28nm, business from AMD that they can be happy for at least another 4 or 5 years before the main long term agreement is over in 2024. That overall agreement with GF terminates in 2024 and then AMD will have met its spinoff agreement in full with AMD’s former fab division that became the company now called Globalfoundries.

I still think that AMD will be contacting some future work with GF for some Polaris Based OEM GPU parts used widely in those budget PCs consumers see so much of at costco and other big chains. The embedded market that AMD is a part of may still want to use GF’s FD-SOI plainer process for the automotive and embedded markets and 16nm, 14nm, and 12nm are going to still be long lived process nodes just like 28nm was and still is.

AMD is also adding higher clocked Zen/Naples variants to its product portfolio with that Epyc 7371, and maybe AMD will start adding some higher clocked 24/32 core Epyc Variants to its offerings in order to increase its Zen-1 based Epyc/Naples ASPs before Epyc/Rome is fully vetted/certified for production server/HPC workloads.

That 14nm GF process is getting more mature but I do not see AMD attempting to use GF’s 12nm/14nm nodes for anything but consumer CPUs/GPUs that are for the OEM market after AMD’s transition to 7nm is complete. Any Ryzen Pro Branded 14nm CPUs or APUs will still be in production for 2-3 years also owing to the fact that Ryzen Pro targets the business PC/Laptop OEM market that sell in volume to enterprise customers.

So Zen-1 based Epyc/Naples and any Ryzen Pro Branded 14nm and 12nm CPUs and APUs for the business OEM market get extended product availability guarantees and 3 year warrenties also. So GF will be busy all around with Epyc/Naples and any Zen-1/Zen+ based Ryzen Pro APUs and CPUs for 2-3 more years if not longer. And the usual Polaris based 14nm/12nm SKUs for the low end OEM PC market will still be Polaris based for years to come.

GF has got a good 5 years before they have to worry about any AMD wafer starts beginning to decline to only smaller numbers. GF is going after the upper mid teir CPU and automotive/industral Processor markets with its FinFet and FD-SOI plainer processes at 14nm and 12nm for finfets and 22nm FD-SOI and also 28nm customers. GF are selling to VIS a Globalfoundries fab in Singapore.

It looks like someone from

It looks like someone from Mubadala read me… :o)

“VIS To Acquire GLOBALFOUNDRIES’ Fab 3E In Singapore”

http://www.vis.com.tw/visCom/servlet/newsServlet?id=692&enable_en=Y&enable_ch=N

Actually I don’t know if it is a good deal for GlobalFoundries but the cash is welcome to invest in more strategic assets such as new materials (e.g. silicon-germanium alloys) to overcome the physical limits of foundries.

GF is out of the cutting edge

GF is out of the cutting edge process business so unless it involves FD-SOI or any 12nm+ process node IP, GF is not going to be making any investments that are not related to production for potential 12nm+ clients in the FinFit process or the FD-SOI finfet or plainer processes.

If anyone of GF clients wants to go lower or leading edge then that’s TSMC, Samsung etc. GF could always license from Samsung/others if the client can broker a deal and GF’s 14nm process node was licensed from Samsung with AMD brokering that deal.

Mubadala wants to see a return on its investments in GF and that comes with more wafer starts and more clients for its 12nm and above process nodes! I’m sure that Mubadala is shopping around for a buyer for GF but who knows if that will pan out. Only those with the big bucks can play at 7nm leading edge and leading materials chip/fab production.

GF is targeting specific markets that do not need any 7nm/below wafer production so automotive and industral processors and even low end smart phone and other devices where 28nm to 12nm is sufficient. GF only has until 2024 bofore AMD has no contractual obligation once GF’s overall spinoff agreement with AMD expires.

GF will be doing wafer starts for AMD until 2024 and probably after under some less limiting terms and conditions. The rest is going to be up to GF to bring in the needed clients to prosper after 2024.

AMD’s GF spinoff is done with the setting sun after 2024 when that larger longer term spinoff deal expires!

And Chipman did you not read the other post directly above yours:

“GF has got a good 5 years before they have to worry about any AMD wafer starts beginning to decline to only smaller numbers. GF is going after the upper mid teir CPU and automotive/industral Processor markets with its FinFet and FD-SOI plainer processes at 14nm and 12nm for finfets and 22nm FD-SOI and also 28nm customers. GF are selling to VIS a Globalfoundries fab in Singapore. ”

“GF are selling to VIS a Globalfoundries fab in Singapore.”[see there that’s already been stated and it’s for that cash for sure]

Mubadala Mubadala who cares, Mubadala Mubadala who cares!

There ain’t nor rhyme or reason to chipman!

GlobalFoundries isn’t dead

GlobalFoundries isn’t dead yet!

Even if AMD move to TSMC’s 7 nm node (only for CPU/GPU but not chipsets) which didn’t prove anything yet, it doesn’t mean GlobalFoundries can’t compete with TSMC providing a turnkey solution including custom wafers (strained silicon, silicon-germanium alloy, etc) for specific high performance or low power circuits at more conventional nodes.

Actually the DDR5 market could be an opportunity to feed GlobalFoundries but I’m not sure if Mubadala digested the 7 nm scam in order to continue with them.

GF’s did not have the funds

GF’s did not have the funds or the business to Justify what that 7nm node would have cost them and that 7nm R&D cost was bleeding GF dry of cash. GF made the wise decision and chose to focus on the process node IP that they already had! And Mubadala wanting some return on their investment in GF was the primary reason that GF got out of 7nm.

GF does not possess the patent IP to get into the memory business that’s already controlled by Samsung, Micron, and SK Hynix and a few others.

GF is a foundry services providor not a memory/processor maker. GF does not have the patent IP for anything but some limited SERDES and Fabrication IP and chip packaging IP.

So GF’s business model consists mainly of providing Wafer atarts for the clients who do have the IP/IP licensing for chip designs and other processor related IP.

Really you do not even understand that market for 7nm very much and are mostly spouting off nonsense. Only those fab companies with 10’s of billions of dollars to invest can make it to 7nm and below. Such are the costs of the leading edge node to actually develop. GF only has the funds to constiue at 12nm and that FD-SOI process along with its 28nm and 14nm(Licensed from Samsung AMD) Related business. That chip fab that was sold off becsue GF needs that money to continue operating in the fab services martetplace that GF has chosen to pursue!

GF lacks the funds for anything bleeding edge and they have only the funds to provide fab services on the IP that GF already has. GF only needs to sale enough wafer starts to keep their fabs operating at as close to 100% capacity as possible so they can generate the revenues necessary to stay in business. So that’s GF goal to continue selling wafer starts unitl that wafer capacity is saturated and then GF can think about rasing the capitol for some new wafer line production capacity/equipment.

“GF does not possess the

“GF does not possess the patent IP to get into the memory business that’s already controlled by Samsung, Micron, and SK Hynix and a few others.”

GlobalFoundries doesn’t need any license to manufacture for its clients.

“So GF’s business model consists mainly of providing Wafer atarts for the clients who do have the IP/IP licensing for chip designs and other processor related IP.”

Indeed captain obvious!

“Really you do not even understand that market for 7nm very much and are mostly spouting off nonsense. Only those fab companies with 10’s of billions of dollars to invest can make it to 7nm and below.”

Actually, you don’t want to acknowledge that GlobalFoundries deceived its main investor (aka Mubadala), pretending to be able to manufacture 7 nm chips for AMD at an effective cost, in the same way they did it for 14 nm chips before taking a license for the Samsung’s 14 nm process.

Thus, it’s not a matter of pocket depth but investment efficiency!

Just look at chipman’s

Just look at chipman’s Mubadala obsession and chipman thinks that Globalfoundries is some R&D juggernaut that siilar to IBMs R&D division or the former Bell Labs at its peak of innovation.

Ol chipman thinks he’s picking up some wavelengths that imparts some special ability to chipman alone but, in fact, that’s just the coil whine from some el-cheapo electronic device that chipman purchased at the flea market.

Wafer starts and some limited fab process node IP is all that GF has now and GF’s no longer in the leading edge process node race. Poor GF has had to sell off a fab and exit out of one market in order to turn its business financials around. FD-SOI production for some clients and 12nm finfet for some others is what GF has and only 5 more years before AMD’s larger spinoff wafer supply agreement is done and over for good. GF’s still has 28nm node offerings also for even lower speced device production.

GF is a niche market player now that it’s out of the Bleeding edge process node race. But sufficient business is to be had with AMD for the next 5 years and with GF’s remaining client base that do not necessarily need any leading edge fab node sercices. GF’s 12nm node is not bad at all for any of its 14nm clients to transition over to. GF has kept its 12nm node’s BEOL the same as that Licensed from Samsung 14nm node’s BEOL so that makes it much more easy for GF’s/any of Samsung’s 14nm clients to go with GF’s 12nm node.

Hell even AMD could possibily rework some Epyc/Naples updates using GF’s 12nm process and bring an updated line of Epyc/Naples higher clocked SKUs to market for workstation usage if AMD wanted. AMD’s still getting better binned 14nm Zen/Zeppelin 14nm DIEs to put out that Epyc 7371 higher clocked Epyc/Naples 16 core part. Who Knows what options AMD could take while it waits for its Epyc/Rome parts to be fully vetted/certified for production workloads and start shipping in volume.

AMD could still take Epyc/Naples and use that to fill out some lower cost server/workstation offerings even with Epyc/Rome in full production. GF’s going to be producing Epyc/Naples Zen/Zeppelin wafers for 3+ more years and possibily longer depending on Epyc/Naples demand. AMD should really begin to offer some higher clocked 24/32 core Epyc/Naples variants because that represents a price segement that’s higher than the older Epyc/Naples lower clocked parts while the lower clocked Epyc/Naples parts could have their MSRPs lowered some more to better compete with the lowest price segements of Intel Xeon Parts offerings.

GF should be wooing AMD to maybe begin producing Zen/Zeppelin based Epyc/Naples+ variants on GF’s 12nm process and offer AMD the incentives via some volume wafer price reductions to make it worthwile for AMD to do so. Epyc/Rome, if its performance metrics match or exceed Intel’s offerings for things like single Core IPC and higher clock rates, are not going to be as affordable as the Epyc/Naples offerings were at introduction.

So maybe some Epyc/Naples+ 12nm refresh and the the older 14nm Epyc/Naples lower clocked variants slotted in to some even lower market segement. Epyc/Rome is not going to come down in pricing until the Zen3 generation based server SKUs are ready for volume production.

Edit: siilar

to: similar

Time

Edit: siilar

to: similar

Time for new eyeballs!

“The amendment provides AMD

“The amendment provides AMD full flexibility for wafer purchases from any foundry at the 7nm node and BEYOND without any one-time payments or royalties.”

http://ir.amd.com/news-releases/news-release-details/amd-reports-fourth-quarter-and-annual-2018-financial-results

Taking a step back I find the wording a bit tricky as usual from AMD. They say BEYOND to say more advanced nodes than 7 nm, which leads me to the conclusion that AMD still have to pay penalties for less advanced nodes such as 14/12 nm.

It means AMD still count on its current portfolio to feed GlobalFoundries…

It’s the revenue growth more

It’s the revenue growth more than any large profit currently that matters most to Wallstreet/Long term Investors! That and AMD getting that middle single digit server market share of a server market that has a $75 billion yearly TAM(total addressable market).

Lisa Su fruther projects that AMD’s Epyc server market share will reach 10% in 4 to 6 business quarters. So that’s at least 10% of the server market share(See quoted earnings call transcript Q/A below) and looking at how Epyc/Naples has been recieved and how many design wins have already been announced for Epyc/Rome based supercomputers/HPC/server systems that 10% server/HPC market share will be reached closer to 4 business quarters that 6 business quarters.

So AMD is getting plenty of revenue growth from its Epyc sales and that also pulling in the Radeon Instinct/Radeon Pro WX server market AI/Compute GPU accelerator sales along for the ride with AMD’s Vega 20 based Compute/AI offerings earning revenues since Q4 of 2018.

The earnings call transscrtpt has a little more information on how Epyc sales are doing than that Enterprise, Embedded, and Semi-Custom segment accounting unit figures show. And that’s because the Epyc numbers are mixed in with the Console semi-custom numbers and the other accounting unit numbers. Console sales are at a cyclical low point so the Epyc sales are/have been helping that EESC unit’s figuers from looking worse.

AMD’s server CPU/Pro GPU revenues are where the real revnue growth and higher gross margin figures will be coming from mostly with Ryzen/Threadripper sales bringing up the line along with mostly the mainstream GPU marker sales. Flagship GPUs are never that much of the total market.

.

.

.

Also, I’m totally suprised at how many Lisa Su interviews with the technology press have not produced any questions regarding AMD’s Discrete Mobile Vega/4GB of HBM2 offerings that appear to be only available on Apple’s Macbook Pro SKUs. Why Anandtech did not even think to ask Lisa Su about that and when the non Apple PC Market could expect to similar Discrete Mobile Vega/4GB HBM2 variants, ore even the status of any diecrete mobile Navi/4GB-HBM2 variants in 2019.

From the NextPlatform article:

” “Fourth quarter server unit shipments more than doubled sequentially based on growing demand for our highest end, 32-core Epyc processors with cloud, HPC, and virtualized enterprise customers,” Su explained on the call yesterday after the market close with Wall Street analysts. “As a result, we believe we achieved our goal of mid-single-digit server unit share exiting 2018. We had another strong quarter of cloud adoption, highlighted by industry leader Amazon announcing new versions of their most popular EC2 computing instances powered by Epyc processors. Businesses can easily migrate their AWS instances to AMD and save 10 percent or more based on the technology advantages of our platform. Microsoft Azure also announced general availability of their AMD based storage instance in the quarter, as well as a new HPC instance powered by Epyc processors that is 33 percent faster than competitive X86 offerings.”

Su called out some HPC system wins, including clusters based on Epyc processors going into Procter and Gamble, the US Department of Energy (the NERSC-9 “Perlmutter” system), and the University of Stuttgart, and notably a system at Lawrence Livermore National Laboratory that employs both Epyc processors and Radeon Instinct GPU accelerators that will be employed for data analytics and machine learning workloads. While there has been a fair amount of tire kicking and testing among enterprise customers and HPC centers said Su, it is the hyperscalers and cloud builders who are driving the shipments of Epyc processors at this point, and it is these same customers who will be at the front of the line for the Rome Epycs, which are socket compatible and which will provide a big bump in performance when they are launched in the middle of this year and ramp in the second half. “(1)

Earnings call Transcript from Seaking Alpha:

“Vivek Arya

Lisa, I’m curious as you look back at 2019 and the success you had with EPYC, the initial success with EPYC. What was the mix of cloud versus enterprise? And then how do you think it trends in 2019, because of all the concerns around slowdown in cloud CapEx and so forth. And as part of that, if you could share with us what your market share assumptions are as we exit the year on EPYC?

Lisa Su

So as we look through 2018, we were pretty pleased with our progress on EPYC. And coming off of the fourth quarter, actually it was a fairly strong fourth quarter for us and in fact that we doubled the number of units for our server business. And when you look at that mix, it is more cloud weighted. So we had some large deployments that went online here in the fourth quarter and that was positive for us. That being said that we’re making nice progress in the enterprise and HCP side of the business too. We’ve had a number of wins in the quarter, as well as going into 2019.

So as we look into 2018, I would expect that the early Rome deployments will also be cloud based. It will be the first ones, but we have a strong set of enterprise platforms. And as I mentioned earlier it’s the breath of the OEM platforms that gives us good confidence that we were going to a broader set of workloads and having broader coverage in the market. In terms of share assumptions we will have to see how the markets and year play out. But I think what we’ve said before is that after reaching the mid-single digit market share in the fourth quarter of 2018, we would expect it would take another four to six quarters to reach 10% market share. And I think we’re still in that range.” (2)

(1)

“AMD Nails Its Epyc Server Targets For 2018”

https://www.nextplatform.com/2019/01/30/amd-nails-its-epyc-server-targets-for-2018/

(2)

“Advanced Micro Devices, Inc. (AMD) CEO Lisa Su on Q4 2018 Results – Earnings Call Transcript”

https://seekingalpha.com/article/4236505-advanced-micro-devices-inc-amd-ceo-lisa-su-q4-2018-results-earnings-call-transcript

Thanks for the break down

Thanks for the break down Josh. Gonna use all my human powers to wait so I can buy a Navi based video card.

RX 580s are so inexpensive

RX 580s are so inexpensive for what you get. Plus 2 free games for the next few weeks.

As much as I agree, and dig

As much as I agree, and dig that like 200 price for a RX580 8gb. My PC gaming soul really needs to upgrade from my crap 1080p monitor to a 1440 and I think a bit more hardware than a RX580.

Currently using a friends old GTX 770 with a watercooling loop.

Ryzen 5 1600

16gb of ram.